2024 Trends Report

We are pleased to report that C&E’s 2024 Scholarly Journals Market Trends report has been released! The report is an essential read for editors, editorial boards, boards of directors, society leadership, and anyone else looking for an in-depth review of the scholarly journals market today.

Benchmarking for Physical Sciences, Engineering, and Mathematics Journals

Join C&E’s 2024 Journal Metrics Benchmarking study to see how your journals compare to peers on editor compensation and workload, editorial office resourcing, submission trends, transfer success rate, turnaround times, cost/revenue per article, research integrity checks, and more. This study is conducted only every 2–3 years, so this is your last chance to participate before 2026.

Reproducibility and Bibliometric Databases

C&E’s David Crotty wrote a Scholarly Kitchen post this month discussing lessons learned in exploring the many bibliometrics databases available, and why reproducibility is complicated..

Retrenchment

1

Bibliometric databases are lagging – it takes time for the millions of articles each year to be accurately indexed, and the numbers bounce around for a while as corrections are made and lost articles found. This is why one of the last things we did in assembling C&E’s just-released Scholarly Journals Market Trends 2024 report was to bring in analysis of 2023 data, as mid-year 2024 seemed a reasonable point to start fully trusting the 2023 numbers. And those numbers reflect what appears to be the early stages of a significant market shift.

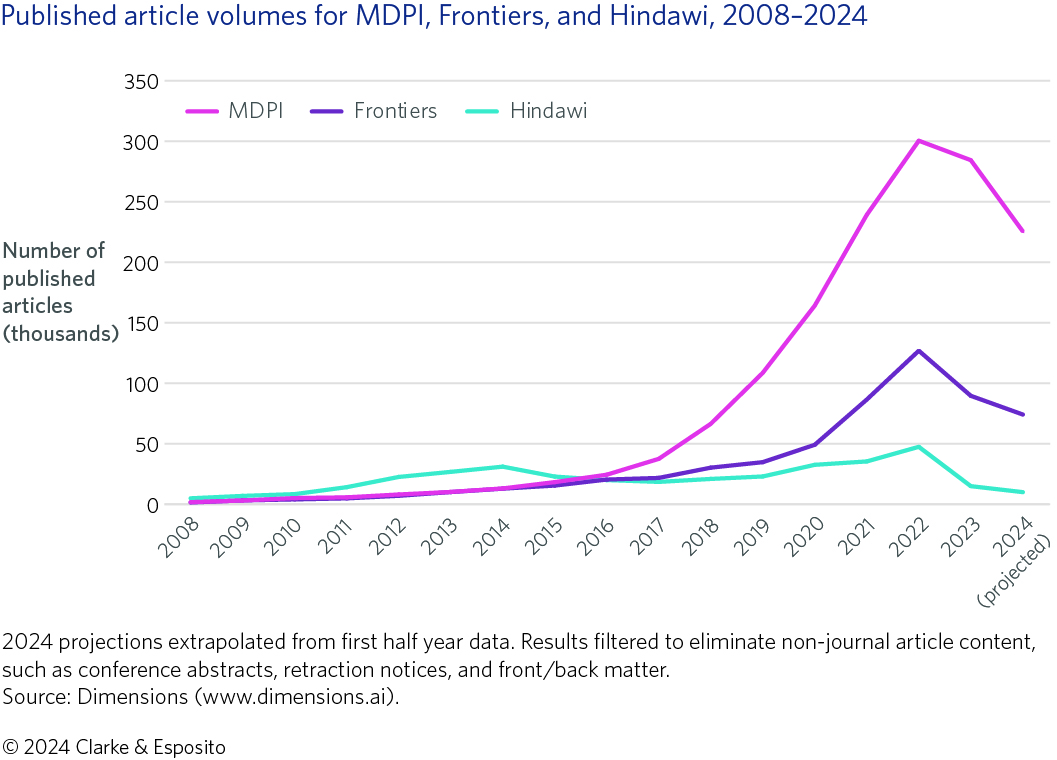

Beginning in the late 2010s, the most remarkable story in professional and scholarly publishing has been the rapid rise of “born open access” (born-OA) publishers, particularly MDPI and Frontiers, and to a lesser extent, Hindawi. These born-OA publishers had no legacy subscription publications and could instead optimize their practices to meet new market conditions. According to Dimensions (an inter-linked research information system provided by Digital Science, www.dimensions.ai), Frontiers went from publishing around 1,300 articles annually in 2008, to 18,000 in 2017, to more than 125,000 in 2022. MDPI’s growth was even more remarkable over the same timeframe, starting at around 1,700 articles in 2008, to a little over 37,000 in 2017, to just under a staggering 300,000 articles in 2022. Over this period, Frontiers grew from being the 110th ranked journal publisher as measured by article output to inhabiting the 6thspot. MDPI, meanwhile, leapt from 91st to 3rd place.

Hindawi’s growth over this same period was impressive but trailed that of its two peers. In 2008, Hindawi published around 4,800 papers. This had grown to over 18,000 in 2017 and peaked at just over 47,000 in 2022. Hindawi’s growth was, however, significant enough that Wiley paid a premium to acquire the publisher in 2021. But its growth came to an abrupt end after 2022. In September 2022, Retraction Watch revealed that Hindawi’s output was riddled with fraudulent papers, largely from paper mills exploiting the publisher’s special issue growth strategy. The full extent of the problem and its implications for Wiley would not be known for another six months, when a March 2023 earnings call set off a shockwave that carved off $400 million from Wiley’s stock value in a single day and ultimately caused the publisher to retire the Hindawi brand entirely.

The most notable outcome of the Hindawi fiasco, however, may prove to be not its impact on Wiley, but on MDPI and Frontiers. Hindawi had borrowed its special issue growth strategy from its born-OA siblings, who had both deployed special issues as the rocket fuel that powered their ascents. Shortly following public awareness of the trouble with Hindawi, both Frontiers and MDPI saw a significant decrease in published output.

Where MDPI had a robust first half of 2023, growing article volume by nearly 20% compared with the first half of 2022, the second half of 2023 saw a decline of 14% in volume compared with the same period the previous year. Frontiers appears to have been affected even earlier in the year, with a 15% decline in article output in the first half of 2023, followed by a 21% drop in the second half.

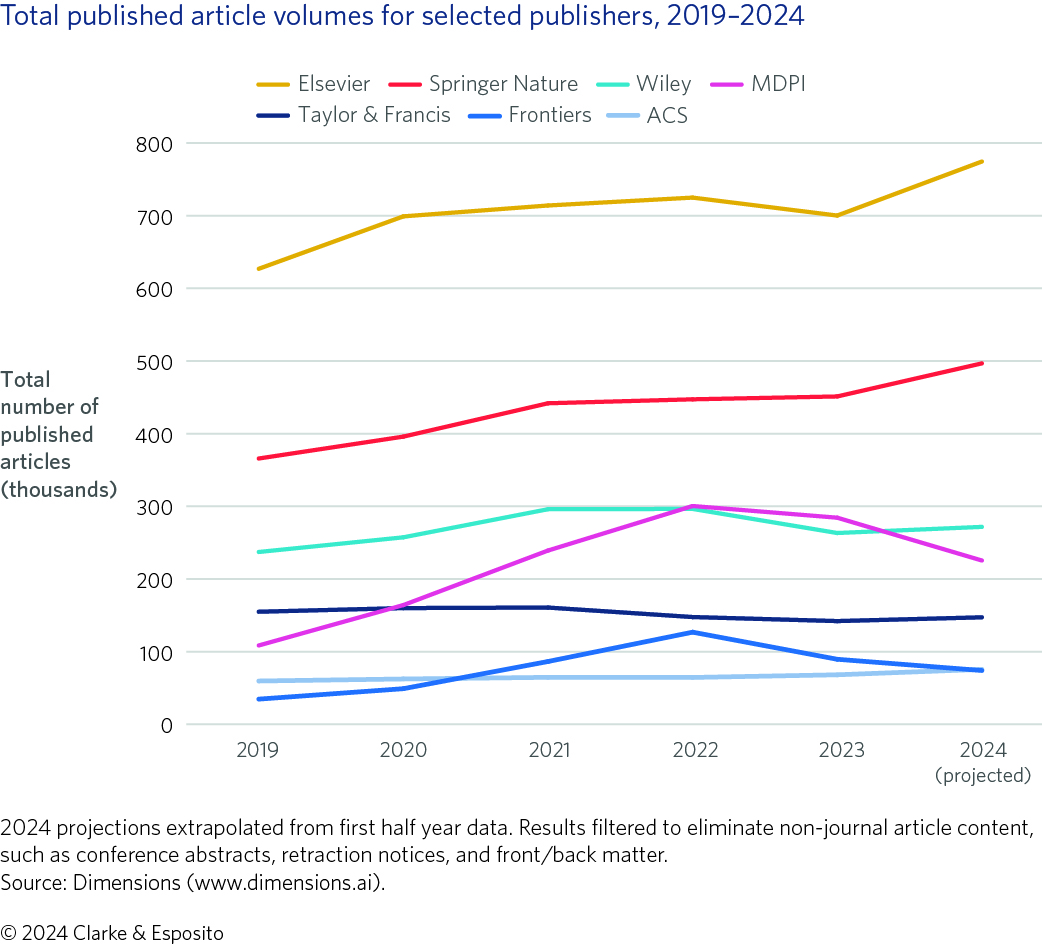

These trendlines continue into 2024. Although the numbers are preliminary and may change over time, MDPI is down 30% (close to 50,000 articles) as compared with the first half of 2023; Frontiers is down 29% compared with the first half of 2023 (which was already down from 2022). These decreases are beginning to add up. Were 2024 to have ended on June 30th, Wiley – which has been relatively flat in terms of publication output excepting the growth provided by the Hindawi acquisition – would move ahead of MDPI to reclaim its spot as the 3rd largest journal publisher by article output. MDPI’s 10 largest journals have all fallen off considerably year-on-year, ranging from a drop of 12% (Journal of Clinical Medicine) to a decline of 85% (International Journal of Environmental Research and Public Health, formerly the second largest journal in the world, now delisted by Clarivate).

The impact on Frontiers has been even more dramatic. Where the publisher looked poised to surpass Taylor & Francis (T&F) for the 5th spot based on article output, it now appears it will fall to 10th, behind IEEE, Wolters Kluwer, the American Chemical Society (ACS), and Sage. Frontiers’ highest-volume journals from 2023 are all much smaller in 2024, ranging from a 19% decline (Frontiers in Public Health) to a 38% decline (Frontiers in Oncology). At the beginning of this year, Frontiers let go around 30% of its workforce in response to the drop in output.

Notably, the declining outputs at MDPI and Frontiers are not indicative of an overall drop in the market, as the total number of papers published in the first half of 2024 appears to have increased by just over 3% from the same period in 2023.

So where are all the papers going, and why? We can answer the first part of this question and speculate about the second.

As to where the papers are going, the big winners so far are the two biggest publishers: Elsevier and Springer Nature. Elsevier is up 14% and Springer Nature up 17% in publication output in the first half of 2024. ACS appears to be on an upward trend as well, growing by over 12% year-on-year. Other publishers seem to be benefiting too; we have heard anecdotally from several publishers that their submissions are up by double digits and they attribute this entirely to the shift away from MDPI, Frontiers, and Hindawi.

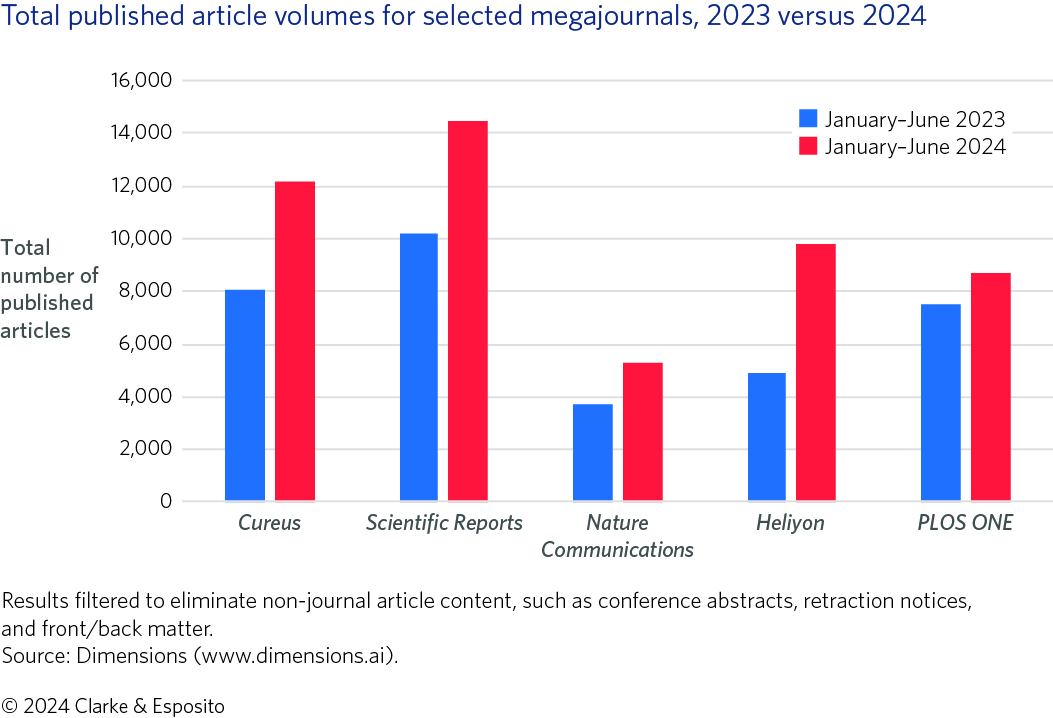

Megajournals in particular are showing remarkable levels of growth, with Springer Nature’s Cureus, Scientific Reports, and Nature Communications all exhibiting greater than 40% growth year-on-year. Elsevier seems to have finally figured out Heliyon, its broad megajournal that launched in 2015 and meandered for nearly a decade before a sudden near-tripling in output in 2023, and an even more impressive near-doubling indicated by early 2024 data. After years of steady decline in output, PLOS ONE seems to be another beneficiary of MDPI’s and Frontiers’ struggles, showing a 16% year-on-year increase in 2024.

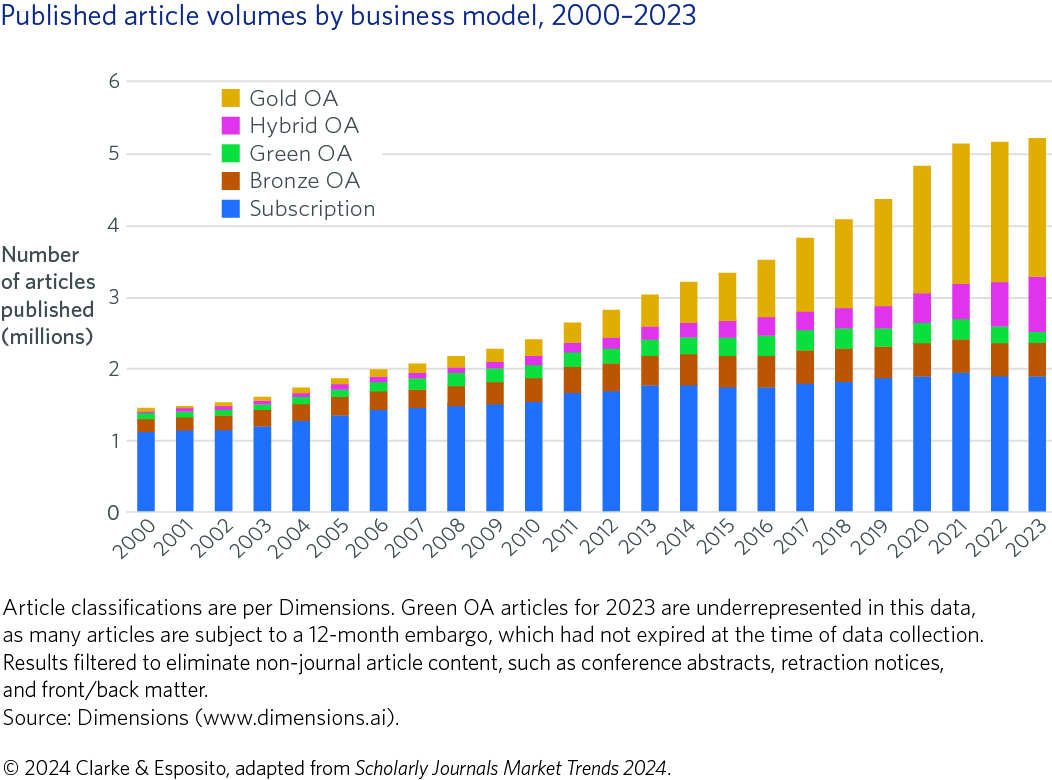

Outside of megajournal growth, the other early beneficiary of the pull-back from the born-OA publishers is the hybrid journal. Fully OA journal output declined 1.7% from 2022 to 2023, whereas hybrid OA grew by 28%. The move away from fully OA journals and toward hybrid journals (largely driven, we assume, by transformative agreements) perhaps marks another retrenchment rather than the envisioned OA revolution.

As to why the market shift away from the leading born-OA publishers is occurring, we can only speculate that it is in part due to increased research integrity controls at Frontiers and MDPI, implemented to avoid the same fate as Hindawi. And in part due to decreased submissions to these publishers amidst reputational concerns associated with special issues. It is possible that Chinese watchlists and the recent changes in China’s publishing policies may also play a role.

While the “Return of the Big Brands” has long been predicted, it is unclear how long this retrenchment will last. While we suspect that MDPI and Frontiers will ultimately emerge as stronger publishers with more sustainable, albeit much slower, growth rates, the timetable for such a turn-about is unclear. Both publishers are in a challenging position. As we have noted previously, the pure-play OA model is more precarious than the subscription (and hybrid) model (and especially the durable Big Deal). It is unclear the extent to which Frontiers’ reduction-in-force was reactionary versus anticipatory and whether further reductions at either Frontiers or MDPI (who to our knowledge has not announced layoffs to date) may be required. The math is unforgiving. MDPI has published 50,000 fewer papers in the first half of 2024 as compared with last year. At an average of CHF 1,258 (US $1,491) per article, this is a decline of over $74.5 million in just the first half of the year – factoring in waivers and discounts, it is somewhat less but still a very large number. And yet, any reduction in head count comes just as more editorial scrutiny is required. This is a strain that all publishers are facing, but pure-play OA publishers have much less room to maneuver due to the proportionate drop in revenue associated with any decrease in output.

Federal Purpose

2

Both bills call on the OSTP to instruct agencies “not to limit grant recipients’ ability to copyright, freely license, or control their works,” with the House of Representatives bill specifically blocking the use of the Federal Purpose License, which reads as follows:

Federal agencies require specific rights to fulfill some aspects of the Nelson Memo. The National Library of Medicine (NLM), for example, receives author manuscripts in various formats. If NLM then posts articles in PubMed Central, it needs the right to make the works publicly available, as well as to create derivative works by making formatted and linked XML versions. But many authors and publishers see the wording of the Federal Purpose License as being far too vague and overreaching for these use cases.

As it is currently written, federal agencies could significantly alter an author’s paper, potentially omitting or changing results in sensitive areas (e.g., climate change, or gun violence) to make them better fit the administration’s views on the subject. Some have noted that the Federal Purpose License is in some ways more liberal than even the CC BY licenserequired by some funder policies as it does not demand attribution.

Publishers we’ve spoken to are also concerned about the open-ended ability to “authorize others to do so,” which creates threats to both research integrity and publisher business models. A federal agency could, for example, authorize private companies to use its repository for AI-training purposes, potentially harming a publisher’s earnings from such activities or an author’s rights to make that decision themselves.

As noted in June’s issue of The Brief, this is not the first time the US Congress has raised questions about the White House’s policy. As the White House has failed to provide Congress with an actual economic analysis (as required by law), the House appropriations bill contains language entirely blocking federal funds from being used to “implement, apply, enforce, or carry out” the Nelson Memo policies.

As we move closer and closer to the finalization of agency policies (December 2024) and the first implementations (January 2025 for the National Science Foundation), many questions remain to be answered.

In other OSTP news, and perhaps indicative of differing agendas within the organization, new security rules were issued last month for research institutions receiving federal funding. These rules include cybersecurity programs designed for a world of “fierce military and economic competition,” meant to stop the “transfer of government-supported R&D to countries of concern.” These regulations seem at odds with the OSTP’s imminent open science policies, which are meant to make all that government-supported R&D publicly available to anyone who wants it.

Researchers Finding Their Voice on OA

3

An essential input that has largely been absent from the planning of OA policy is the collective voice of those most directly affected by funder requirements – the researchers themselves. As more and more poorly planned policies bring about more and more unintended consequences, impacted researchers are beginning to raise their voices.

This month, the UK’s Research Excellence Framework (REF) rescinded planned requirements for academic books to be made OA. The policy U-turn was chiefly driven by the uproar raised by researchers and their institutions through the REF’s open consultation on the policy, which was seen by the academic community as both “unaffordable” and “excessively bureaucratic.”

The world of academic research is highly rigorous and data-driven, so it is perhaps not surprising to see researchers demanding similar rigor and analysis from policymakers. Faculty from the Massachusetts Institute of Technology (MIT) addressing the Nelson Memo policies point out that “…there has been no concerted effort to anticipate the implications of the policy-driven changes as they relate to associated costs; the benefits from greater immediate dissemination; and the consequences for the research community and the public at large.” The editorial calls for the launch (and funding) of a research agenda “to elucidate how changes in policy and practice will affect the communication of research results.”

To be clear, while there doesn’t seem to be a widespread resistance to OA, or open science in general, among the emerging voices, there is clear and growing dissatisfaction regarding currently favored approaches, which Science noted this month are neither fair nor sustainable.

If OA was easy and obvious solutions existed, they would already be in place. With such a complex and thorny set of problems, the increasing number of researchers joining the policy conversation and the call for actual analysis and planning are welcome developments.

Briefly Noted

4

Scale is a particularly helpful component of success in the OA journals market, giving the largest publishers an advantage in negotiating transformative agreements. The benefits of being in such agreements become evident when looking at two recent reports. Germany’s DEAL consortium has released an overview of results of their 2019–2023 transformative agreements with Elsevier, Wiley, and Springer Nature. While the three publishers were responsible for around 26% of the papers published worldwide in 2023, the report shows that they published 50% of the papers from German authors. Although this concentration was likely due to a wide variety of factors, the role that Projekt DEAL agreements played in pushing authors toward these publishers can’t be dismissed. Elsewhere, Springer Nature’s 2023 Open Access Report shows that 44% of the company’s 400,000-plus research articles were published OA. This figure is supported by Springer Nature’s transformative agreements, which are responsible for 44,500 articles – a 46% increase from 2022 and just over 10% of Springer Nature’s total article output.

cOAlition S has released the final version of its pricing framework. As we noted upon the release of the draft version (in September 2023) and discussed in last month’s The Brief, list prices for journal subscriptions and article processing charges (APCs) have mostly become irrelevant in the current market, where publications are purchased in bulk through packages of journal collections and discounted APCs are paid increasingly through transformative agreements.

An account of one peer reviewer’s experience with several versions of the same paper at multiple journals suggests further issues at MDPI. This month MDPI also apparently purchased advertising space via “sponsored content” in Politico through an advertorial calling support for OA a “moral imperative.” Although labeled as sponsored content, the article contains no conflict-of-interest notice regarding its author, MDPI CEO Stefan Tochev.

Duncan MacRae, Director of Editorial Strategy and Publishing Policy at Wolters Kluwer, offers an excellent explanation essential for understanding the new batch of Journal Impact Factors (JIFs) issued in the 2024 Journal Citation Reports. As we noted in June’s issue of The Brief, the overall size of the literature indexed by Clarivate decreased in 2023 from the previous year, resulting in fewer overall citations and largely declining JIFs. Duncan notes that what really matters is relative performance compared with related journals.

Licensing of scholarly materials for use by AI is becoming more widespread as The Bookseller reports that deals are in place for materials from Wiley, T&F, and Oxford University Press (OUP). T&F has a second agreement in place beyond the original $10 million licensing arrangement with Microsoft, bringing their 2024 partnership earnings to $75 million. Wiley has added an additional $23 million in AI licensing revenue to its already reported $21 million deal. Despite continued outcry from authors, it is perhaps worth noting that Wiley states that their authors are “set to receive remuneration for the licensing of their work based on their ‘contractual terms’.,” Regardless of the inclusion of licensing terms in author contracts, Nature reports that if an author’s work is online, then it’s already being used for AI training, whether part of a licensing deal or not.

OUP’s George Woodward offers a helpful set of questions that journals and societies should be asking their publishers. We recommend supplementing this information with Michael Clarke’s articles “The Journal Publishing Services Agreement: A Guide for Societies” and “Navigating the Big Deal: A Guide for Societies.”

In other AI news, the European Association of Science Editors (EASE) is seeking comment on its draft set of Recommendations on the Use of AI in Scholarly Communication.

The Digital Public Library of America has teamed with the Independent Publishers Group to create a new route for library acquisitions of ebooks and audiobooks, offering libraries outright ownership of their purchases rather than licensing agreements.

As if publishers didn’t have enough new integrity monitoring responsibilities (and expenses) on their plates, we at The Brief have been seeing a rise in the use of “hijacked journals” to defraud authors. Multiple publishers are reporting fake websites advertising their journals to trick authors into submitting to the wrong place, and an increased number of letters from authors who mistakenly think their paper (which was never submitted to the actual journal) was accepted. Liverpool University Press offers an update on their experiences, and it’s worth noting that these sorts of scam are not limited to journals, but appear to target book authors as well.

Another area of additional effort and costs for journals is getting caught in the middle of legal disputes between researchers. Retraction Watch details two feuds that required journals (PNAS and Journal of Clinical Imaging Science) to revise and republish recent papers.

Cory Doctorow has written a blog piece about how MIT faculty are faring without access to Elsevier’s Big Deal. Despite the title of the post – “MIT libraries are thriving without Elsevier” – most of the piece is dedicated more generally to describing scientific and scholarly publishing. Mind, one of the scholarly journals that MIT faculty likely still have access to (as it is published by OUP not Elsevier), published a paper in 2018 on the topic of “epistemic trespassing,” the phenomenon of writing or speaking on a topic in which one is not an expert. Warren Buffet and Charlie Munger coined a more pithy term, “circle of competence,” to describe the same concept. Doctorow has provided a helpful reminder of the dangers inherent in venturing outside one’s circle of competence.

Personnel moves this month include former ProQuest CEO Matti Shem Tov taking the reins at Clarivate, and Gregg Gordon stepping down after 30 years at SSRN.

Has PowerPoint become (shudder) cool? The Washington Post seems to think so. We at The Brief lean more toward Edward Tufte’s viewpoint that it should be used with caution.

***

There are many true statements about complex topics that are too long to fit on a PowerPoint slide. – Edward Tufte